Bad credit can put you in a tough spot when looking for student loans. This is especially true if you are looking at private student loans. But what about federal student loans? Can I take out federal student loans with a poor credit history? How?

What is Considered a Bad Credit Score?

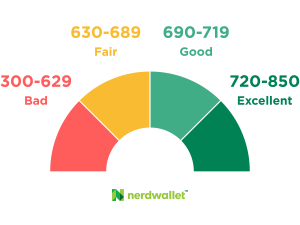

The FICO credit scoring model ranges from 300 to 850, with 300 being the lowest score you can get and 850 being the highest score you can get. What is considered a “bad” credit score will vary depending on the lender you talk to. Typically, anything under 630 is considered high risk to most private lenders.

Source: Nerdwallet

Can I Get a Federal Student Loan with Bad Credit?

The good news is that most federal student loans don’t require a credit check to qualify. So, even with an adverse credit history, you have options. To see if you are eligible for these loans, fill out the FAFSA. There are four different types of federal loans you might get depending on your situation.

Direct Subsidized Loans

Direct Subsidized Loans are available only to undergraduate students with financial need. So, you’ll have to show that you have financial need to get this loan. Your answers from the FAFSA will be used to determine whether you do or not.

The government will pay interest on these loans while you are in school. Once you graduate, you’ll be in charge of interest payments. Additionally, you do not need to pass a credit check to get this loan.

Direct Unsubsidized Loans

Direct Unsubsidized Loans are available to both undergraduate and graduate students. You won’t need to show financial need to get this loan. So, it’s open to a lot more people. On the flip side, the government won’t pay interest on these loans while you are in school. The interest will accumulate unless you make payments on them, which if you can, is a good idea. These also don’t require a credit check to qualify.

Direct PLUS Loans

Direct PLUS Loans are available to graduate/professional students and parents of students. Like unsubsidized loans, you’ll be responsible for the interest. Unlike subsidized and unsubsidized loans, however, these do require an adverse credit check. If you fail that, you’ll need an endorser or a creditworthy cosigner to qualify. Additionally, there is also an extra application you need to fill out outside of the FAFSA to get this loan. Check with your school about the application process.

Direct Consolidation Loans

Direct Consolidation Loans allow you to combine all of your federal loans into one. Your new interest rate will be the average of all your previous loan interest rates. While you may not get a lower interest rate, doing this helps you to more easily manage your student debt. It can even lower your monthly payment. There is also no cost to consolidating your loans. And you don’t need to go through a credit check to do so.

Ways to Improve Your Credit Score Before Taking Out a Loan

While bad credit isn’t as big a deal for most federal student loans, it will matter if you’re taking out a PLUS loan. So, you’ll want to improve your credit score before you take out a PLUS loan so you can pass the credit check. There are different things you can do to help boost your credit score.

Take a look at your debt and payments. Making your payments on time and paying off your debt is good for your credit score. Doing this will show that you are reliable and can handle your debt, which makes you less of a risk. In fact, making on-time payments can even help raise your credit score a little in just six months.

So, continue paying all of your bills on time, and try to pay off any outstanding debt, such as credit card debt, if you can.

Keep open lines of credit you already have and refrain from opening new ones. The length of your credit history is an important factor to determining your credit score. The longer you stay with the same credit account, the better you look. Refrain from closing any current lines of credit you have because it will lower the length of your credit history and impact your score. Likewise, opening new accounts will cause a hard inquiry into your credit which will temporarily hurt your credit score. So, unless you really need to, stray from closing current or opening new accounts.

Regularly check your credit report. Keeping track of your credit report is important to understand your financial situation, but also to check for errors, fraud, and identity theft. Even a small error on your credit report can significantly hurt your score, so it’s important to check fairly often. There are many financial institutions, such as banks and credit card companies, that offer free credit reports. If yours don’t, go to the Annual Credit Report website to get a free credit report from each of the three major credit bureaus. You are, by law, entitled to these reports yearly.

Final Thoughts from the Nest

Bad credit and student loans seem like the worst combination in the world. And you may be stressing that it’s your current situation. Luckily, you can still take out federal student loans to help cover your school expenses. And even from those, you have different loan options depending on your circumstances.

Now, if federal student loans don’t cover all your expenses, there are still a variety of private student loan options that can help cover your remaining college costs. Sparrow can help you find private student loan options for people with bad credit. Just fill out the Sparrow application to be matched with what you qualify for at top lenders. You can even save and compare your favorite lenders before moving forward. Since we partner with 15+ lenders, there’s no doubt you’ll find a good loan for you.