Consumer

Products built to simplify and automate borrowing.

Business

Products built to power seamless marketing.

Newsstand

The latest updates and insights from our team.

Resources

Helpful tools to get your questions answered.

Deciphering your student aid package is already like reading IKEA furniture instructions. Confusing.

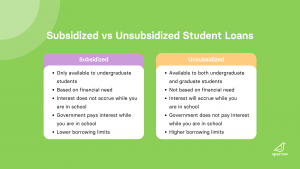

One of the biggest points of confusion for prospective college students is the difference between subsidized and unsubsidized loans. Understanding the difference is important as it impacts your interest, repayment, and overall student debt.

Both Direct Subsidized and Direct Unsubsidized Loans are forms of federal financial aid offered by the U.S. Department of Education to support students in paying for higher education.

Neither Direct Subsidized or Direct Unsubsidized loans require you to make payments while in school.

Direct Subsidized loans are available to undergraduate students who are deemed eligible. The US Department of Education pays the interest on Direct Subsidized loans during certain periods such as:

During these periods, interest won’t accrue and your principal balance won’t grow (this means that your loan amount isn’t getting bigger – ideal scenario!).

In order to qualify for Direct Subsidized loans, you must meet all of the federal student aid requirements. Filling out the FAFSA will allow you to see if you qualify.

It’s important to note that Direct Subsidized loans are only available to undergraduate students who demonstrate financial need. This is one of the major differences between Subsidized and Unsubsidized loans. Each respective university will determine how much students can borrow in Direct Subsidized loans as the amount cannot exceed the determined financial need.

You are also only eligible to receive Direct Subsidized loans for 150% of your program length. This means that, for example, if you are in a 4-year program, you can only receive Direct Subsidized loans for 6 years (4 * 150%).

There is a limit in how much you can borrow in Direct Subsidized Loans. The following chart breaks down the annual limits which are based on your year in school.

Year in School

Direct Subsidized Loan Limit

Undergrad Year 1 Annual Limit

$3,500

Undergrad Year 2 Annual Limit

$4,500

Undergrad Year 3 Annual Limit

$5,500

Lifetime Subsidized Loan Max

$23,000

Unsubsidized loans differ from subsidized loans in that interest begins to accrue as soon as the loan amount is disbursed (sent out) and you are responsible for that interest. So, if you use a Direct Unsubsidized loan to pay for your freshman year of college, interest will accrue on that loan for the entirety of your college career and beyond.

Direct Unsubsidized loans are a tiny bit more flexible than Direct Subsidized loans in that they are available to both undergraduates and graduate students, and you don’t need to provide financial need in order to secure one.

Similar to Direct Subsidized loans, each university will determine how much you can borrow in unsubsidized loans based on the cost of attendance and the other elements of the financial aid package. So, for example, if the cost to attend your university was covered by scholarships and a Direct Subsidized loan, you might not be able to secure a Direct Unsubsidized loan.

Unlike subsidized loans, unsubsidized loans don’t have a maximum eligibility period. They do, however, have a borrowing limit just like subsidized loans. This is where things could get a bit confusing, so stick with us.

Unsubsidized loan limits are based on your year in school, but also factor in how much you received in Direct Subsidized loans and your dependent status. So what does this mean?

Let’s use the chart and scenarios below to illustrate this.

Year in School

Dependent Status Students

Independent Status Students

Undergrad Year 1 Annual Limit

$5,500

$9,500

Undergrad Year 2 Annual Limit

$6,500

$10,500

Undergrad Year 3 Annual Limit

$7,500

$12,500

Graduate/Professional Degree Annual limit

N/A

$20,500

Subsidized

$31,000 $57,500 for undergrads

$138,500 for graduate/professional students

Scenario 1: Sara, a 1st year undergraduate student who filed as an independent

($9,500 – $1,500 = $8,000)

Scenario 2: Michael, a 3rd year undergraduate student who filed as a dependent

($7,500 – $2,000 = $5,500)

If you want to skip pre-qualification and apply directly with a lender, you can do so by clicking Apply below.

In general, Subsidized loans will be a better option as interest won’t be accruing as it would with Unsubsidized loans.

However, if you aren’t eligible for Direct Subsidized loans because you don’t demonstrate enough financial need, then Direct Unsubsidized loans will be the better option (and your only option likely).

Either way, federal loans in general will likely be the best loan option in comparison to private lending options. Thus, you should take out what you can in federal loans before dipping into private loan options.

Federal Direct Subsidized and Unsubsidized loans are great options to explore if you are offered them. If federal loans don’t cover your financial need entirely, it may be time to explore private loan options.