Whether you’re well-versed with student loans or know nothing about it, we all want to make the smartest, most cost-effective decision when it comes to our financial circumstances.

Refinancing your student loan is a great financial decision and a feasible option for student borrowers, even if you have poor credit.

Refinancing, in simple terms, is a trade. You can refinance, or “trade”, the mortgage to your house, car loan, and student loan for a better option.

Most people refinance their student loans because they want to reduce the overall amount of the loan or get the lowest interest rate possible.

What Credit Score Do You Need to Refinance?

Generally, most loan servicers require a credit score of 620 and up in order to refinance your student loan. Sparrow’s lending partners typically have a minimum credit score requirement of 650 or higher if you want to refinance your student loan.

If your credit score doesn’t meet the minimum requirement, exploring your cosigner options and adding a cosigner to the loan is your best bet to qualify.

When Should You Refinance Student Loans?

If you’re debating whether or not you should refinance your student loan, ask yourself these questions:

- Has your credit score improved, qualifying you for competitive interest rates and loan options?

- Are you paying high interest rates, but know there are better, lower interest rate options than your current interest rate on the market?

- Do you want to extend your repayment term and pay smaller amounts over a longer period of time?

- Are you paying a variable interest rate, meaning that your interest rate fluctuates based on the benchmark interest rate or index?

If you answered yes to even one of these questions, consider refinancing your loan and applying with a cosigner to bolster your chances.

Best Student Loan Refinance Companies for Bad Credit

Sparrow partners with refinancing companies that want to help student borrowers with bad credit get the best option that they can. The following are our top picks:

Arkansas Student Loan Authority

The Arkansas Student Loan Authority (ASLA) is an Arkansas state entity that provides student loan refinancing for Arkansas residents. ASLA has a minimum credit score requirement of 670.

College Ave offers student loan refinancing with competitive rates, flexible repayment terms, and strong customer service. College Ave’s student loan refinance offering is best if you are seeking a more flexible repayment term that allows you to find a loan that matches your budget. To qualify for a refinance loan with College Ave, you will need a credit score in the mid-600s.

Earnest’s student loan refinancing option is great if you are seeking competitive interest rates, unique borrower perks, and flexible repayment options that allow you to find a loan that matches your budget. Earnest has a minimum credit score requirement of 650.

ISL is a nonprofit lender that offers both private student loans and student loan refinancing. ISL’s student loan refinancing is best if you haven’t graduated and want generous forbearance policies. ISL has a minimum credit score of 670.

LendKey is an institution that offers educational funding to undergraduate and graduate students. By connecting borrowers with a network of 100+ lesser-known credit unions and community banks, LendKey allows you to work with smaller lenders with low rates and good customer service, rather than traditional lending institutions. LendKey has a minimum credit requirement of 680. It’s best if you want generous cosigner release and forbearance policies.

SoFi is one of the largest student loan refinance companies in the industry. With competitive interest rates, a diverse set of repayment options, and exclusive member benefits, SoFi is a good fit for borrowers with an associate’s degree or higher or borrowers with a high income. SoFi has a minimum credit score of 650.

What if I Don’t Get Approved For Refinancing My Student Loan?

If you don’t get approved for refinancing your student loan, don’t lose hope. It is still possible for you to reapply to refinance your loan. Under the Equal Credit Opportunity Act, you have a right to request a written explanation of why your application was denied from your lender. This will allow you to either reapply with new lenders or reapply for the same loan once you’ve addressed the discrepancies in your application.

Consider taking the following steps to increase your chances of being approved for a refinance loan.

Step 1: Add a cosigner.

A cosigner is an individual that “co-signs” the loan with you, meaning that if you fail to pay off the loan, your cosigner is contractually obligated to pay it off on your part. When you add a cosigner with a higher credit score to your loan, the lender will factor in their credit score to the rates and terms you’re able to access. Thus, having a creditworthy cosigner is advantageous as it can help you qualify for a loan you otherwise wouldn’t on your own.

As for cosigners, you won’t be contractually obligated until the entire loan is paid off, depending on the circumstances. The requirements to qualify for cosigner release vary, but the borrower needs to sign off on a cosigner release form, meet a certain number of on-time payments, and have their credit history reviewed.

Step 2: Improve your credit score.

Improving your credit score is the most intuitive fix if you’re trying to get approved to refinance your student loan. A poor credit score is between 300-579, a fair credit score is between 580-669, a good credit score is between 670-739, a very good credit score is between 740-799, and an excellent credit score is between 800-850.

You’ll want to bump your credit score up a range (or more, if possible!). Here are some steps you can take to improve your credit score.

- Pay your bills on time. 35% of your FICO credit score consists of your payment history, or your ability to pay your bills on time. This is the most important factor to your credit score, so stay on top of paying off any outstanding debt or bills you may have.

- Pay off your debt. Your credit score also considers your credit utilization ratio. Your credit utilization ratio is how much credit you’ve spent versus how much credit you have available. For example, let’s say you have two lines of credit. One line of credit has a $500 credit limit, while the other has a $750 credit limit. In total, you have $1,250 of available credit. Now let’s say you’ve used $20 on your first line of credit, and $600 on your second line of credit, meaning you owe $620. $620 is 49.5% of $1,250, which isn’t a great credit utilization ratio. You’ll want to have a credit utilization ratio of 30% or less.

- Limit new credit accounts. Applying for a new credit line requires a hard inquiry, which can damage your credit score temporarily. To prevent your score from dropping, stick to the credit lines you have currently. If you really need to open a new line of credit, make sure to explore your options in a 45-day period. Banks don’t count three new credit applications as three separate hard inquiries if you submit them within a 45-day period.

- Don’t close any credit card accounts. Your length of credit history is 15% of your FICO credit score, so the longer credit history you have, the better it is for your credit score.

- Pay attention to your credit reports. It’s important to check your credit reports for any misinformation, fraud, error, or possible identity theft. You’ll want your credit reports to be 100% accurate when trying to qualify for a new loan.

Step 3: Boost your cash flow or cut down on expenses.

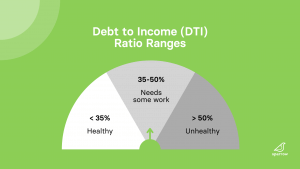

Lenders measure your creditworthiness with the debt-to-income ratio (DTI). Your DTI tells lenders the ratio of how much you owe to your monthly gross income. For example, let’s say you pay $250 a month for your student loan and $450 for your auto loan.

That’s $700 in monthly debt payments. Now let’s say your gross monthly income (the total you earned before taxes) is $1,500. $700 is roughly 46% of $1500, so your debt-to-income ratio is 46%.

A healthy DTI is 34% and under, an okay DTI is 35%-50%, and an unhealthy DTI is over 50%.

Alternatives to Refinancing

Okay, let’s say that refinancing your student loan hasn’t been working out for you, but you still need lower monthly payments or a longer repayment term.

Consider the following options to get the benefits of refinancing without actually refinancing your loan.

Opt for an income-driven repayment.

An income-driven repayment option is for federal student loans only. An income-driven repayment option is a type of federal repayment plan that readjusts your monthly student loan payment based on your income and family size.

The federal government offers four different income-driven repayment plans that all cap your loan payment between 10% and 20% of your discretionary income (total income after taxes) and forgives your remaining loan balance after 20-25 years of payment.

- Revised Pay As You Earn Repayment Plan (REPAYE Plan)

- Pay As You Earn Repayment Plan (PAYE Plan)

- Income-Based Repayment Plan (IBR Plan)

- Income-Contingent Repayment Plan (ICR Plan)

If federal income-driven repayment is an option for you, make sure to read up on each plan and determine which one is the best fit for you.

Opt for federal student loan consolidation.

Federal student loan consolidation is combining multiple federal student loans into one federal loan. This allows you to extend your loan term, lower your monthly payment, get rate discounts, and potentially qualify for an income-driven repayment plan.

On the flipside, federal student loan consolidation warrants longer pay periods, higher interest accumulation, and the loss of specific borrower benefits.

Closing Thoughts From The Nest

Don’t be discouraged if you have to refinance your student loan but have a bad credit score. There are many options available to you as long as you stay deliberate and informed in your journey to securing a new student loan.

Sparrow’s many refinancing partners can help you refinance your student loan. Submit an application with us today to see your options.

Sparrow’s goal is to give you the tools and confidence you need to improve your finances. Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. While we make an effort to include the best deals available to the general public, we make no warranty that such information represents all available products.